1c advance report return of accountables. Return by the accountable person of the amount of the unspent advance. Daily and travel expenses in the advance report

The issuance of funds to accountable persons can be made in cash or non-cash.

Cash withdrawal

The issuance of cash to accountable persons is formalized using the document “Cash Expenditure Order”. This document is available from the “Cashier” menu.You can also go to the “Cash expenditure order” in the “Cash” tab of the program function panel.

To issue from the cash register cash accountable person, you should use the document transaction type “Issuance to an accountable person”.

To issue from the cash register cash accountable person, you should use the document transaction type “Issuance to an accountable person”.  In order for funds to be issued correctly, the accountable amount and the accountable person must be indicated. The reporting amount is entered manually by the user, and the reporting person is selected from the “Individuals” directory.

In order for funds to be issued correctly, the accountable amount and the accountable person must be indicated. The reporting amount is entered manually by the user, and the reporting person is selected from the “Individuals” directory.  The “Print” tab contains the details necessary for printing the cash receipt order form.

The “Print” tab contains the details necessary for printing the cash receipt order form. “Issue:” – copies the line “Accountable person”;

“Base”, “Application” – filled in manually by the user

“By:” – copies information about the identity document of the accountable person” from the individual’s card.

After the document is processed, the cash balance in the cash register decreases and the debt to the individual who received the accountable amount increases.

After the document is processed, the cash balance in the cash register decreases and the debt to the individual who received the accountable amount increases.

Issuance of non-cash funds

The issuance of non-cash funds is formalized using the document “Write-off from the current account.” This document is available from the “Bank” menu and is located in the “Bank Statements” journal. The “Bank Statements” journal can also be found in the “Bank” tab of the program’s function panel.

The “Bank Statements” journal can also be found in the “Bank” tab of the program’s function panel.  In order to issue non-cash funds to an accountable person, the transaction type “Transfer to an accountable person” should be used.

In order to issue non-cash funds to an accountable person, the transaction type “Transfer to an accountable person” should be used.  In order for the money transfer operation to proceed correctly, you need to correctly fill out the following mandatory details of the document “Write-off from the current account”:

In order for the money transfer operation to proceed correctly, you need to correctly fill out the following mandatory details of the document “Write-off from the current account”: - Amount – the amount of funds transferred to the accountable person.

- Accountable person is the employee to whom the accountable amount is transferred. This detail is selected from the “Individuals” directory.

- Recipient – the employee to whom the accountable amount is transferred. This detail is selected from the “Counterparties” directory.

- Recipient's account – the account to which the accountable amount will be transferred. Account information is available from the counterparty card in the “Accounts and Agreements” tab.

- Purpose of payment – filled in manually by the user.

After execution, the document reduces the balance of funds in the current account and also increases the debt of the accountable person.

After execution, the document reduces the balance of funds in the current account and also increases the debt of the accountable person.

Debt of accountable persons

After funds are issued to accountable persons, a debt is formed to employees. The status of this debt can be monitored using the report “Turnover balance sheet for account 71”. From this report it is clear that Marina Viktorovna Ivanova must report in the amount of 1000 rubles, and Victoria Pavlovna Simonova was transferred 2000 rubles.

From this report it is clear that Marina Viktorovna Ivanova must report in the amount of 1000 rubles, and Victoria Pavlovna Simonova was transferred 2000 rubles. Preparation of an advance report

An advance report is drawn up in order to cover the debt of the accountable person, that is, to reflect the expenditure of the funds issued to him for the needs of the enterprise.The document "Advance report" is available from the "Cash" menu.

In order for the “Advance report” document to be processed correctly, the following mandatory document details must be correctly filled out:

In order for the “Advance report” document to be processed correctly, the following mandatory document details must be correctly filled out:  After this document is completed, the debt of the accountable person is reduced.

After this document is completed, the debt of the accountable person is reduced.

Registration of overspending of funds

Often there is a situation when the accountable person does not have enough money issued to him in order to pay the expenses for the needs of the document. In this case, the accountable person is forced to use his own funds, which the company is obliged to return to him. The amount of overexpenditure is also reflected in the balance sheet.

The amount of overexpenditure is also reflected in the balance sheet.  Refunds of funds spent in excess of those issued are made using the documents “Expense cash order” or “Write-off from the current account” using the same technology as the issuance of funds to an accountable person.

Refunds of funds spent in excess of those issued are made using the documents “Expense cash order” or “Write-off from the current account” using the same technology as the issuance of funds to an accountable person. Registration of cash balance

A situation may also arise in which the issued funds are not fully spent. In this case, the accountable person retains part of the accountable amount, which the employee must return to the enterprise. The debt of the reporting person can also be seen in the balance sheet.

The debt of the reporting person can also be seen in the balance sheet.  As a rule, the return of the balance of the advance is reflected in the document “Cash receipt order”. This document is available from the “Cashier” menu.

As a rule, the return of the balance of the advance is reflected in the document “Cash receipt order”. This document is available from the “Cashier” menu.  This document can also be found in the “Cashier” tab of the program’s function panel.

This document can also be found in the “Cashier” tab of the program’s function panel.  To return the balance of accountable amounts, use the transaction type of the document “Return from an accountable person.”

To return the balance of accountable amounts, use the transaction type of the document “Return from an accountable person.”  To correctly process this document, you must correctly fill out the following details:

To correctly process this document, you must correctly fill out the following details: 1. Amount – the amount of the balance of accountable funds, which is deposited into the cash register (filled in manually by the user).

2. Accountable person – an employee who returns the balance of the accountable amount (selected by the user from the “Individuals” directory).

The “Print” tab is designed to correctly generate the printed form of this document.

The “Print” tab is designed to correctly generate the printed form of this document. “Accepted from” is copied from the “Accounting Person” line.

“Base” and “Attachment” are filled in manually by the user.

After the document is processed, the debt of the accountable person decreases, and the cash balance increases.

The dynamics of the debt of the accountable person can be tracked in the report “Turnover balance sheet for account 71”.

The dynamics of the debt of the accountable person can be tracked in the report “Turnover balance sheet for account 71”.

This article discusses the features of the regulatory regulation of accounting for settlements with accountable persons in accounting, tax accounting, as well as the procedure for reflecting business transactions for accounting for settlements with accountable persons in the program "1C: Accounting 8" (rev. 2.0). The article was prepared by M.S. Suchkova.

- on the way;

- for renting residential premises;

Regulatory regulation of settlements with accountable persons

In the course of their activities, organizations can issue cash to their employees for travel and business expenses based on the order of the manager. In such situations, employees are accountable persons. The procedure for issuing funds for reporting and reporting is established by the Central Bank of the Russian Federation (Procedure for conducting cash transactions in the Russian Federation, approved by decision of the Board of Directors of the Central Bank of Russia dated September 22, 1993 No. 40). The head of the organization determines the amount of accountable amounts and the terms for which they are issued. Accountable persons, within three days after returning from a business trip or upon expiration of the period for which the funds were issued, must submit a report on the use of funds (according to the unified form No. AO-1 “Advance report”) and attach supporting documents.

In accordance with Article 166 of the Labor Code of the Russian Federation, a business trip is a trip by an employee by order of the employer for a certain period of time to carry out an official assignment outside the location permanent job. A permanent place of work is recognized as the location of an organization in which work is stipulated by an employment contract. The procedure for sending an employee on business trips, both on the territory of the Russian Federation and on the territory of foreign states, is regulated by the Regulations on the specifics of sending employees on business trips, approved by Decree of the Government of the Russian Federation dated October 13, 2008 No. 749. If sent on a business trip, the employer is obliged to reimburse the employee for the following expenses:

- on the way;

- for renting residential premises;

- additional expenses associated with living outside the place of permanent residence (per diem);

- other expenses incurred by the employee with the permission of the employer.

When sending an employee on a business trip to the territory of a foreign state, the following expenses are additionally reimbursed:

- for obtaining a foreign passport, visa and other travel documents;

- to obtain compulsory health insurance;

- mandatory consular and airport fees;

- fees for the right of entry or transit of motor vehicles;

- other mandatory payments and fees.

Accounting for settlements with accountable persons is kept on account 71 “Accounting for settlements with accountable persons”. The debit of account 71 in correspondence with the credit of cash accounts reflects the issuance of cash amounts for reporting. Spent accountable amounts are reflected in the credit of account 71 in correspondence with expense accounts or other accounts, depending on the nature of the expenses incurred.

Reflection of travel expenses in tax accounting

In accordance with paragraphs. 12 clause 1 of Article 264 of the Tax Code of the Russian Federation, business travel expenses are classified as other expenses associated with production and sales. For income tax purposes, the following expenses may be taken into account:

- travel of the employee to the place of business trip and back to the place of permanent work;

- rental of residential premises, including the employee’s expenses for paying for additional services provided in hotels (with the exception of expenses for service in bars and restaurants, expenses for room service, expenses for the use of recreational and health facilities);

- daily allowance or field allowance;

- registration and issuance of visas, passports, vouchers, invitations and other similar documents;

- consular, airport fees, fees for the right of entry, passage, transit of automobile and other transport, for the use sea channels, other similar structures and other similar payments and fees.

From January 1, 2009, the amounts of daily allowance and field allowance are not standardized for income tax purposes (Federal Law No. 158-FZ dated July 22, 2008). The moment of recognition of travel expenses under the accrual method is the date of approval of the advance report (Article 272 of the Tax Code of the Russian Federation).

Amounts of value added tax (VAT) paid on business trip expenses (travel expenses to and from the place of business travel, including expenses for the use of bedding on trains, as well as expenses for renting residential premises) are subject to deduction (clause 7, article 171 of the Tax Code of the Russian Federation). The basis for deducting VAT amounts are invoices or documents confirming payment of the amount of tax withheld by tax agents (strict reporting forms).

In accordance with the Tax Code of the Russian Federation, an employee’s income for the purpose of calculating personal income tax (NDFL) does not include daily allowances paid in accordance with the law Russian Federation, but no more than 700 rubles for each day of a business trip in the Russian Federation and no more than 2,500 rubles for each day of a business trip abroad, as well as actually incurred and documented targeted expenses, for example, travel expenses, expenses for renting residential premises ( Clause 3, Article 217 of the Tax Code of the Russian Federation). When traveling on the territory of the Russian Federation (foreign business trip) with a daily allowance exceeding 700 rubles (2500 rubles) per day, personal income tax must be calculated and paid for an amount exceeding 700 rubles (2500 rubles) per day. If the employee fails to provide documents confirming payment of expenses for renting residential premises, the amount of such payment is exempt from taxation in accordance with the legislation of the Russian Federation, but not more than 700 rubles for each day of being on a business trip in the Russian Federation and not more than 2,500 rubles for each day of being in overseas business trip.

In accordance with paragraph 2 of Article 9 Federal Law dated July 24, 2009 No. 212-FZ, daily allowances, as well as actually incurred and documented targeted expenses for business trips of employees, both within the territory of the Russian Federation and outside the territory of the Russian Federation, are not subject to insurance contributions. If documents confirming payment of expenses for renting residential premises are not provided, the amounts of such expenses are exempt from insurance premiums within the limits established in accordance with the legislation of the Russian Federation.

Keeping records of settlements with accountable persons in the program "1C: Accounting 8" (rev. 2.0)

Let's consider an example of settlements with an accountable person when issuing cash for business needs in the 1C: Accounting 8 program. As an example, let's look at several possible options developments of events.

Example 1

On 04/01/2011, the Primer organization issued employee Ivanov V.D. 10,000 rubles for the purchase of an external hard drive.

In the "1C: Accounting 8" program, this operation is reflected in the document "Cash expenditure order" (main menu item "Cash") with the type of business transaction "Issue to an accountable person." In the document it is necessary to fill out an accounting account, in in this case 50.01, the issued amount is 10,000 rubles. On the “Payment Details” tab we indicate “Accountable person”, which we select from the directory “Employees”, “Ivanov Vladimir Danilovich” and the cash flow item “Issue of funds to the accountable”. The document generates transactions Dt 71.01 Kt 50.01 10,000 rubles. Figure 1 shows the posted document “Cash expenditure order” and the results of its execution.

Rice. 1. Issuance of funds to an accountable person

Option 1. Advance report with unspent amounts

04/08/2011 Ivanov V.D. presented an advance report and documents on the purchase of a disk worth 9,000 rubles. Unspent funds were returned to the cashier.

In the program "1C: Accounting 8" the document "Advance report" is generated (main menu item "Cash"). In the props “physical. person”, indicate the accountable person “Ivanov Vladimir Danilovich”, on the “Advances” tab, select the document according to which the funds were issued. First, select the document type “Cash outgoing order”, then select from the displayed list required document, in our example this is RKO No. 1 dated 04/01/2011, the remaining fields of the table will be filled in automatically. On the “Products” tab, indicate the “nomenclature” of the purchased product, from the “Nomenclature” directory, select “External hard drive”; if it is not in the list, then add it to the directory. We indicate the quantity - 1 piece, price, amount - 9,000 rubles, % VAT - 18%, the VAT amount is calculated automatically - 1,372.88 rubles. To automatically generate an invoice, in the program we indicate the supplier - “Retail store”, put a tick in the “Invoice presented” field, indicate the date and invoice number. We indicate the disk accounting account - 10.09 and the VAT accounting account - 19.03. An example of filling out the Advance Report is shown in Figure 2. As a result of posting the document, the following transactions are generated:

Debit 10.09 Credit 71.01

- 7,627.12 rubles,

Debit 19.03 Credit 71.01

- 1,372.88 rubles.

Rice. 2. An example of filling out the “Advance report”, the “Advances” and “Goods” tabs

The return of the unspent amount (1,000 rubles) is reflected in the 1C: Accounting 8 program using the document “Cash receipt order” with the type of business transaction “Return from an accountable person”, which indicates the returned amount of 1,000 rubles, the accountable person and the type of cash flow funds. An example of filling out the PKO is shown in Figure 3. The document generates the following transactions:

Debit 50.01 Credit 71.01

- 1,000 rubles.

Rice. 3. Receipt cash order

In order to verify that all calculations are reflected in the program correctly, you can draw up a balance sheet for account 71.01 and make a selection for employee V.D. Ivanov. (Figure 4).

Rice. 4. Balance sheet for account 71.01 with selection by employee V.D. Ivanov

Option 2. Advance report with overruns

04/08/2011 Ivanov V.D. presented an advance report and documents on the purchase of a disk worth 11,000 rubles. The organization reimbursed the excess amount.

In this situation, an “Advance report” is generated in the “1C: Accounting 8” program, which is filled out in the same way as in option 1 (Figure 2), only a different cost of the hard drive is indicated. The issuance to the accountable person of the amount of excess expenses over the advance payment issued (1,000 rubles) is formalized by the document “Cash Expenditure Order”, which is filled out as in Figure 1.

Option 3. Advance report with unrefunded amounts

Ivanov V.D. submitted an advance report on 04/08/2011. The manager’s order stated that the amount for the purchase of an external hard drive was provided for the period from 04/01/2011 to 04/07/2011. Cash remaining after purchasing an external hard drive, V.D. Ivanov didn't return it. By order of the manager, it was decided to withhold the remaining funds from the employee’s salary.

Accountable amounts not returned by employees on time are reflected in the credit of account 71 "Settlements with accountable persons" and the debit of account 94 "Shortages and losses from damage to valuables. They are then written off from account 94 "Shortages and losses from damage to valuables" to the debit of account 73 " Settlements with personnel for other operations."

In the 1C: Accounting 8 program, the operation of accepting an external hard drive for accounting is reflected in the document “Advance report” (Figure 2). Operations to reflect shortages are reflected in the document “Operations entered manually.” For this example The following leads must be formed:

Debit 94 Credit 71.01

- 1,000 rubles- reflection of shortage;

Debit 73 Credit 94

- 1,000 rubles - writing off debt for employee shortages;

Debit 70 Credit 73

- 1,000 rubles - deduction of unreturned amount from salary .

Rice. 5 - Write-off of unreturned accountable amount for shortages

Example 2

Advance report for a business trip

Ivanov V.D. was sent on a business trip for 3 days to Moscow to conclude an agreement for the supply of goods (from 05/23/2011 to 05/25/2011). Ivanov V.D. an advance was issued in the amount of 30,000 rubles, calculating the daily allowance of 2,700 rubles (900 rubles * 3 days), rental costs of 12,000 rubles (4,000 rubles * 3 days), plane tickets 15,300 rubles.

05/27/2011 Ivanov V.D. submitted an advance report, a travel certificate, a report on the performance of an official assignment and supporting documents: an invoice for hotel accommodation in Form N 3-G in the amount of 13,500 rubles (4,500 rubles * 3 days) and a check for payment of accommodation; air tickets worth 14,000 rubles. The amounts of VAT paid in the documents are highlighted in a separate line.

The procedure for reflecting operations in the 1C: Accounting 8 program:

1. On May 20, 2011, the document “Cash expenditure order” is generated with the type of business transaction “Issue to an accountable person” (Figure 6). The document generates the posting:

Debit 71.01 Credit 50.01

- 30,000 rubles.

Rice. 6. Issuance of funds to an accountable person for travel expenses

2. On May 27, 2011, the “Advance report” document is generated. On the “Advances” tab, the document for which the advance “Cash receipt order” was issued is indicated. On the “Other” tab, daily allowances, housing rental expenses, and travel expenses are indicated (Figure 7). The document will generate the following postings:

Debit 44.01 Credit 71.01

- 2,700 rubles- daily allowance;

Debit 44.01 Credit 71.01

- 11,440.68 rubles- housing rental costs;

Debit 19.04 Credit 71.01

- 2,059.32 rubles- VAT on housing rental costs;

Debit 44.01 Credit 71.01

- 11,864.41 rubles- travel expenses;

Debit 19.04 Credit 71.01

- 2,135.59 rubles- VAT on travel expenses.

Rice. 7. Reflection of travel expenses in the document “Advance report”

3. On 05/27/2011, the document “Expense cash order” is generated to reflect compensation for overexpenditure on the advance report in the amount of 200 rubles. The document generates the posting:

Debit 71.01 Credit 50.01

- 200 rubles.

4. On May 31, 2011, it is necessary to reflect the accrual of personal income tax on the amount exceeding the norm for daily allowance. The excess amount is: (900 rubles - 700 rubles) * 3 days = 600 rubles. The personal income tax amount is: 600*13%=78 rubles. In the program "1C: Accounting 8" the operation of calculating the amount of personal income tax is reflected as follows:

- The document “Operation entered manually” indicates the posting Debit 70 Credit 68 for 78 rubles.

- If accounting wages is maintained in the program "1C: Accounting 8", then for the purposes of calculating wages and generating personal income tax reports, the amount of excess income and the amount of personal income tax must be entered in the document "Entering income, personal income tax and taxes (contributions) from the payroll", and

- the amount of income (600 rubles) is indicated on the “Personal Income Tax: Income and Taxes” tab (Figure 8),

- the amount of personal income tax (78 rubles) must be indicated on the tabs “Personal income tax at a rate of 13%”, “Personal income tax withheld” (Figure 9, Figure 10).

Rice. 8. Reflection of the amount of income from exceeding the daily allowance standards for personal income tax

Rice. 9. Reflection of the personal income tax amount

Rice. 10. Reflection of the amount of personal income tax withheld

One of the most difficult sections in accounting for government agencies is settlements with accountable persons. In this article I want to look at the most common mistakes made by accountants when keeping records for this section in the 1C program: Accounting for a government institution 8 edition 1.0.

So, the first mistake is the choice of the fourth subaccount for account 208 “Types of settlements with accountable persons”.

This subconto is used for situations where settlements are made using monetary documents (food stamps, etc.). In most cases, payments are made in the usual way - in money. But 1C users fill out this subaccount because the program makes it possible to do this, and diligent accountants are accustomed to filling out all the fields so that the document is processed without errors.

Thus, if calculations based on monetary documents are not used, then the fourth subaccount for account 208 does not need to be filled out!

The second common mistake is the incorrect order of date and time in documents for settlements with an accountable person.

In the picture above, three blocks with these details are highlighted. In a document, not only the date matters, but also the time – hours, minutes, seconds.

The first is the time of the document in the program. It must be the earliest. Then comes the time of documents for issuing money and documents for posting goods or services. It should be slightly later than the document time. And the third is the date and time of the “Advance Report” document, which you print as a primary document - it must be the latest, a difference of at least one second is considered acceptable.

And another common mistake is indicating different subaccounts of account 208 in the documents for one expense report.

It is clear from the text of the error that in the document “Purchase of Materials” the wrong advance payment to the accountable person was selected, so it is not attached to the required document.

Carefully select a subaccount, and all details will be correctly reflected in the document.

So, do not fill out the fourth subconto if payments are made in money. Keep track of time and control which documents are selected as the third subconto.

If these conditions are met, there will be no problems in settlements with accountable persons.

If you need more information about working in 1C: BGU 8, then you can get our collection of articles onAdvance report- this is a document standard form, which confirms the expenditure of the advance, drawn up and presented by the accountable person, supported by documents confirming the expenditure. It reflects information about the amounts received, the actual expenses incurred, the balance of the accountable amounts or their overexpenditure.

Example expenses:

- purchase of materials, OS, goods, gasoline, etc.;

- postage;

- travel and daily expenses;

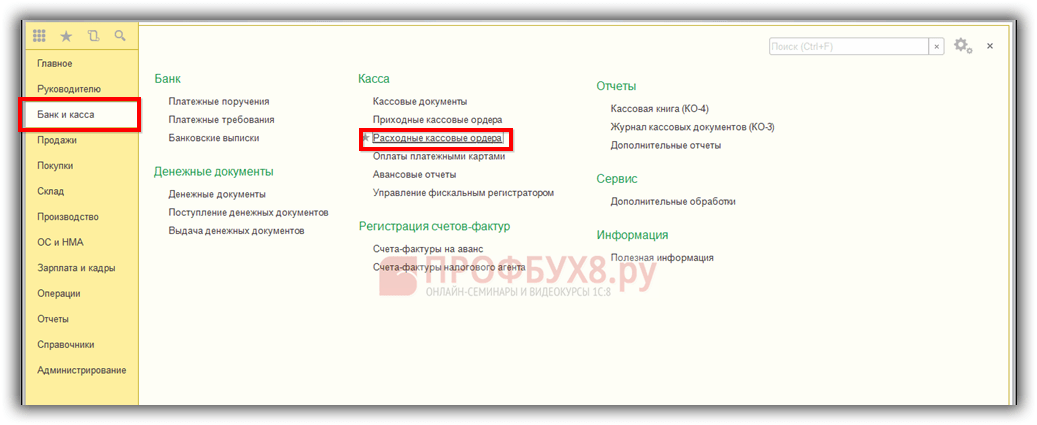

Location of the Advance Report in the 1C Accounting 8.3 program: section Bank and Cashier- group Cash register– document Advance report:

The advance report in 1C 8.3 is drawn up in the currency in which the funds were issued to the employee - the accountable person. That is, if cash settlement was issued to an employee in foreign currency, then the advance report must be reflected in foreign currency.

The advance report in 1C 8.3 is generated in rubles by default. To change the currency, follow the link Edit prices and currency and in the open settings window select the currency:

The document has several tabular parts:

On the bookmark Advances information about the funds issued is indicated and the following documents are reflected:

- Debiting from the current account;

- Issuance of monetary documents:

On the bookmark Goods– funds issued to an accountable person can be spent on the purchase of goods. This tab reflects the following documents presented for the acquired assets:

- Checks;

- Invoices;

- Invoices:

Bookmark Returnable packaging is filled in if the accountable person purchased returnable packaging:

Bookmark Payment. With money, the employee could also pay off any previously existing debts of the organization to counterparties, or pay an advance to the counterparty:

On the bookmark Other All other expenses are reflected:

- Costs of purchasing tickets;

- For services (representational), etc.:

How to make an expense cash order (RKO) in 1C 8.3

To create an Advance report document in 1C 8.3, you need to create a document , which is located in the Bank and Cash Department section, in the journal of cash outgoing orders:

Click the Create button and fill in the required document details:

- Type of operation– select Issue to accountable person;

- In field Recipient we select an employee to whom we will issue funds;

- Specify the amount ;

- Choose Cash item(via Select) – Issuance of funds to the accountant:

- Let's fill in the fields Base and Application:

Posting the document Cash receipt order

Post the document (Post button) and see what transactions have been generated:

Click on the Save and close button. Thus, we carry out and close the cash register in 1C 8.3.

How to fill out an Advance report in 1C 8.3

Let's move on to Advance report and create a new one using the button Create. Fill in the required fields of the document:

- In field Accountable person We indicate the employee of the organization who submitted the Advance report to the accounting department;

- In field Stock We indicate the organization’s warehouse, which will display the materials purchased by the employee;

- Tabular part. On the bookmark Advances through Add enter the advance payment document:

RKO, which was formed earlier:

The employee presented a supporting document - an invoice from the seller. Let's display it on the bookmark Goods Click the Add button and enter information about the purchased product:

- We indicate information about the delivery note and invoice;

- We put a tick in the “SF” field of the supplier.

- We enter the invoice data and after posting the document, it is created automatically by the 1C Accounting 8.3 program:

All that remains is to conduct an advance report.

Let's look at the postings generated by him in 1C:

Monitoring the status of settlements with the accountable person in 1C 8.3

To control the status of settlements with the accountable person in 1C 8.3, it is necessary to create a balance sheet for account 71 in the Reports section:

If there is no debit and credit balance for an employee, it means that he has completely spent the funds that he received for reporting.

On the website you can view the configuration of 1C Accounting 8.3

How to avoid mistakes when preparing an expense report in 1C 8.2 (8.3), see the following video.

An advance report from the accountable person is drawn up, which can be found in the section Bank and cash desk – Cash desk – Advance reports.

In the header of the document you must indicate:

- from- date of preparation of the advance report;

- Accountable person - individual, which provided the advance report.

Reflection of previously issued accountable amounts in the advance report

October 17 Druzhnikov G.P. brought an advance report for previously issued accountable funds in the amount of 30,000 rubles.

If the employee was previously given funds, they should be indicated on the tab Advances .

You can fill out this tab only by selecting documents using the button Add. Advances to accountable persons may be issued in the following documents:

- Issuance of monetary documents type of operation Issuance to an accountable person , for example, if the Organization acquired or transferred them to an accountable person.

- Cash withdrawal type of operation Issuance of accountable personsat , If .

- Debiting from current account type of operation Transfer to an accountable person , If .

In our example, Druzhnikov G.P. an advance in the amount of 30,000 rubles was previously issued.

If advances have not been issued previously, then this tab is not filled in, and reimbursement of expenses to the employee made from personal funds for the needs of the organization, Bukhekspert8 recommends making payments through the “Settlements for other transactions” account.

How to prepare an advance report when purchasing materials and inventory items

Let's look at how to conduct an advance report in 1C 8.3 for the purchase of materials and goods using the example of the purchase of stationery by an accountable person.

- check with allocated VAT for the purchase of stationery from Kontur LLC:

- A4 paper - 5 points at a price of 236 rubles. (including VAT 18%);

If the accountable person has provided primary documents for the purchase of materials, goods or other inventories (MPI), then their list is indicated on the tab Goods .

Additional documents for the inventories for which the employee reported Receipt (act, invoice) no need to create! The posting of materials and goods to the warehouse purchased by the accountable person is carried out by a document Advance report .

On the tab Goods fill in the name, number of inventories and the amount for which they were purchased, as well as data on the submitted VAT, the supplier and the document on the basis of which VAT can be deducted.

Advance report SF. When posting a document Advance fatherT Invoice issued for the amount of VAT entered in the column VAT, which can be taken for deduction.

SF is not included, while the VAT allocated in the primary document is indicated in the column VAT .

As a result of the document Advance fatherT

If the accountant has paid the supplier for the goods, but there has been no delivery, the goods have not arrived at the warehouse, and there is only a receipt for payment, then it is necessary:

- The acquisition of inventory items should be processed through when they arrive at the organization. In this case, nothing is indicated;

- indicate payment to the counterparty on the tab Payment .

Daily and travel expenses in the advance report

Let's look at how to reflect daily allowances and business trip expenses in the advance report using the following example.

Daily allowances in the Organization in accordance with the Regulations on Business Travel are paid at the rate of 700 rubles/day, in total - 4,200 rubles.

- railway ticket (Moscow-Sochi) in the amount of 4,000 rubles. (including VAT 18% - 120 rubles);

- railway ticket (Sochi-Moscow) in the amount of 5,000 rubles. (including VAT 18% - 130 rubles);

- receipt and SF for hotel accommodation in the amount of 9,440 rubles. (including VAT 18%).

Travel expenses (including daily allowances issued to an employee) are indicated on the tab Others .

Services and other costs in the expense report in 1C 8.3 using the example of postage costs

Let's look at how to fill out an advance report in 1C for the purchase of postal services using the following example.

- KKM check for payment of postage in the amount of 354 rubles (including VAT 18%);

All expenses of an accountable person that do not have a material form are taken into account on the tab Other .

The data of the primary document, the name of the costs and their amount, as well as data on the submitted VAT, the supplier and the document on the basis of which VAT can be deducted are entered. Here it is also necessary to show the postage stamps that were used and reflected in accounting as monetary documents.

If the accountant attached to the document Advance report invoice issued to the organization, then you need to check the box SF. If, instead of the SF, documents are attached that correspond to the characteristics of the strict reporting form (SRF), for example, tickets, then you must additionally check the box BSO. When posting a document Advance report a document will be created automatically Invoice issued for the amount of VAT indicated in the column VAT. This amount of VAT can be deducted.

If only a primary document is attached (for example, a cash register receipt), in which VAT is highlighted, then the checkbox SF is not included, while the VAT allocated in the primary document is entered in the column VAT. As a result of the document Advance report such VAT will be written off as expenses not taken into account when taxing profits.

Payment to the counterparty in the advance report

Let's look at how to fill out an advance report in 1C for payment to a counterparty using the following example.

- bank order for Internet payment in the amount of 1,534 rubles.

An employee's advance report for the transfer of an advance or payment to a counterparty is drawn up on the tab Payment .